Global Trade Issues a Worry for Europe’s Plastics Industry

Most European regions and sectors in the plastics industry are looking ahead with a cautious outlook, with a majority of companies concerned about the impacts from global trade conflicts on their business, according to a new survey by PIE – Plastics Information Europe. PIE surveyed more than 200 participants from the plastics industry on business performance, outlooks and concerns.

Almost 30 % expect company performance to worsen in second half of 2019

While 22 % of those surveyed rated business performance as worse in the first half (H1) of 2019 compared to the second half (H2) of 2018, nearly 30 % expect business in H2 2019 to be worse than in the first half of this year. By location, companies in the Nordic region seemed to fare better, with more than 50 % reporting better business performance in H1 2019 compared to H2 2018. The regions with the largest share rating business as worse in a half-year comparison were Spain (35 %) and German-speaking Europe (32 %). Across sectors, plastics processors appeared to fare the best, with almost half rating business as better. Looking ahead, 29 % expect business in H2 2019 to be worse than in H1, with 44 % foreseeing it as staying the same. Businesses in the UK (43 %) and France (37 %) make up the highest shares having an optimistic outlook in H2 2019.

While 22 % of those surveyed rated business performance as worse in the first half (H1) of 2019 compared to the second half (H2) of 2018, nearly 30 % expect business in H2 2019 to be worse than in the first half of this year. By location, companies in the Nordic region seemed to fare better, with more than 50 % reporting better business performance in H1 2019 compared to H2 2018. The regions with the largest share rating business as worse in a half-year comparison were Spain (35 %) and German-speaking Europe (32 %). Across sectors, plastics processors appeared to fare the best, with almost half rating business as better. Looking ahead, 29 % expect business in H2 2019 to be worse than in H1, with 44 % foreseeing it as staying the same. Businesses in the UK (43 %) and France (37 %) make up the highest shares having an optimistic outlook in H2 2019.

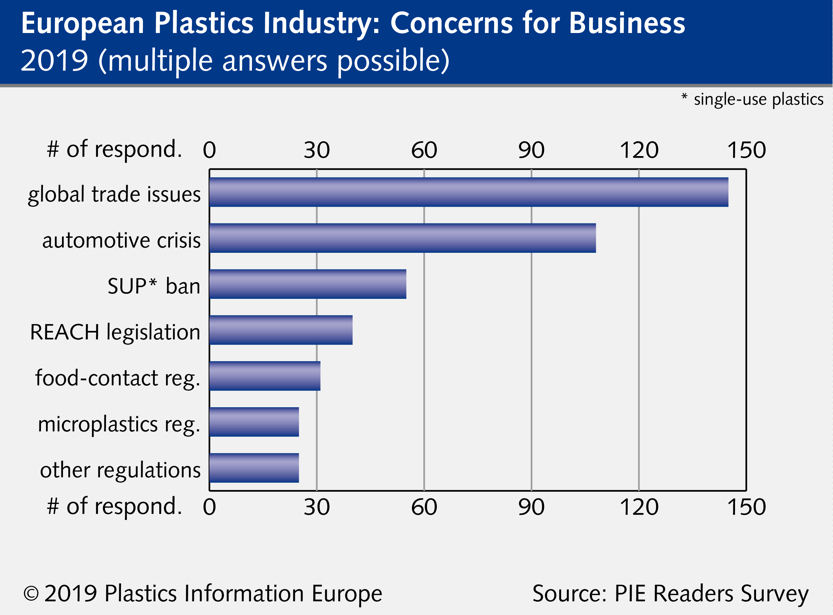

Global trade conflicts are major concern

The effects of global trade conflicts on business were a significant concern for the majority of those surveyed, with 71 % viewing trade conflicts as negatively impacting business performance. Those in distribution and compounding had the largest share seeing negative impacts from trade conflicts (89 %), followed by brand owners (83 %). Around 70 % of plastics processors were seeing negative impacts on business performance.

Effects from weak automotive industry

This year’s crisis in the automotive industry was negatively impacting businesses, either directly or indirectly, for 52 % of those surveyed. Around 40 % saw no impact on business performance, while the remainder saw positive effects. Looking across regions, companies in German-speaking Europe were clearly feeling the crisis, with around 90 % saying business was negatively affected. Only 22 % in the Nordic region witnessed a negative impact from the auto sector’s downturn, and 16 % even saw some good effects on business.

EU plastics-related regulations

For 43 % of respondents, EU regulations were not expected to negatively impact business. The remainder were concerned about the ban on single-use plastics (26 %), REACH regulations (19 %), food-contact legislation (15 %), microplastics regulation (12 %), “other” regulations (8 %) and medical device regulations (4 %). Other regulations that were of concern for the 8 % included CO2 reduction programmes, fallout from Brexit, the WLTP emissions test for cars, a tax on plastic packaging and recycling-related guidelines.

For 43 % of respondents, EU regulations were not expected to negatively impact business. The remainder were concerned about the ban on single-use plastics (26 %), REACH regulations (19 %), food-contact legislation (15 %), microplastics regulation (12 %), “other” regulations (8 %) and medical device regulations (4 %). Other regulations that were of concern for the 8 % included CO2 reduction programmes, fallout from Brexit, the WLTP emissions test for cars, a tax on plastic packaging and recycling-related guidelines.

PIE – Plastics Information Europe

For more than 35 years, PIE has been an invaluable source of information for decision-makers in Europe’s plastics industry. PIE subscribers have access to a print edition twice a month as well as comprehensive online news coverage, including polymer price and market reports, industry news, analysis tools and an online archive. Providing independent market information, the PIE price indices are accepted throughout the industry as a benchmark and embedded in countless supplier contracts. More than 5,500 European companies put their trust in PIE’s data and industry coverage.

For more information, visit www.pieweb.com.

Source: PIE – Kunststoff Information Verlagsgesellschaft mbH (27.11.2019), Photo: Vecoplan